Norway

In Norway, the travel allowance covers sustenance (food and drink), and sustenance only. The tax-free rates are based on the company policy for the Norwegian government, but with a lower rate based on accommodation type. The rule set for trips within Norway are different than the rule set for trips abroad.

References

• Regjeringen.no: Statens reiseregulativ

• Skatteetaten: Forskuddssatser for trekkfri kostgodtgjørelse

Tax-free travel allowance Norway

National: Travel within Norway

Requirements:

• Distance between departure and at least one of the destinations must be at least 15 kilometers.

• The trip must last for at least 6 hours.

• If it is known before the trip starts that it will last for more than 28 days, the ruleset in PM-2013-17: Særavtale om økonomiske vilkår ved endret tjenestested applies from day 29.

◦If there has been a break in the trip, like the employee has been home for the weekend, his stay will continue when he comes back, and not start on day 1 again.

Definitions

• Full day: 24 hours from the start of the trip.

• Night: Between 22.00 and 06.00

• For trips that last more than one full day, each day that lasts for more than 6 hours counts as one full day

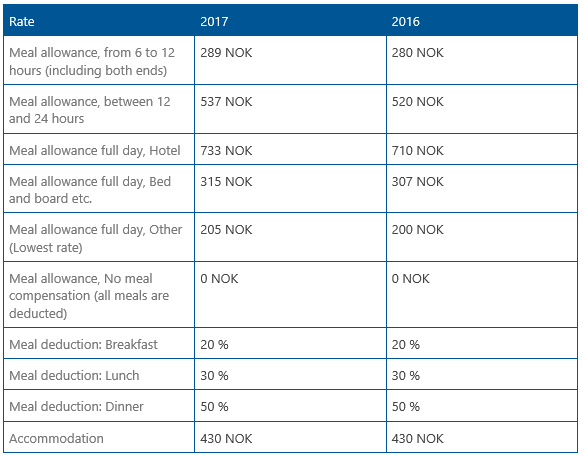

Rates

National: Travel within Norway

Denmark

The Danish Meal allowance covers food, drink and minor costs such as bus-tickets, parking, storing of suite cases etc. The Danish Accommodation Allowance covers accommodation. Danish employers can choose to pay their employees a meal and/or an accommodation allowance instead of the actual costs (documented by receipts).

Tax-free rates

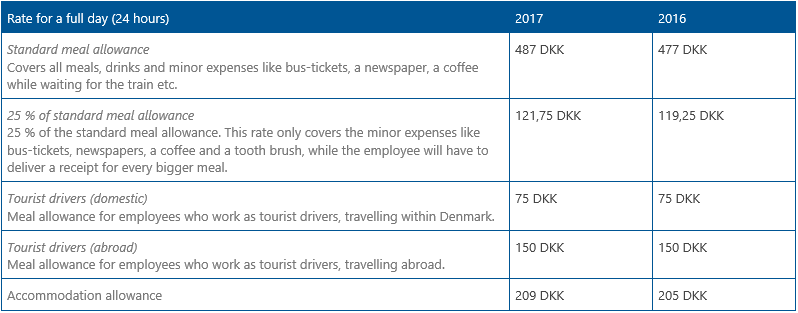

The tax-free rates are decided by the Danish tax authorities for one year at a time, and are:

(Danish travel allowance rates from SKAT: Skattefri rejsegodtgørelse (diæter))

(Danish travel allowance rates from SKAT: Skattefri rejsegodtgørelse (diæter))

Specification

Meal allowance

• The travel must be at least 24 hours for the employee to get the meal allowance.

• After 24 hour, the employee is refunded 1/24 of the full day (24 hours rate) for each started hour.

This means that:

• If the trip lasted for 23 hours and 59 minutes, the employee is not entitled to meal allowance.

• If the trip lasted for 24 hours and 0 minutes, the employee gets: One full day.

• If the trip lasted for 24 hours and 1 minute, the employee gets: One full day and 1 hour.

• If the trip lasted for 47 hours and 1 minute, the employee gets: Meal allowance: Two full days (the 48th hour has started).

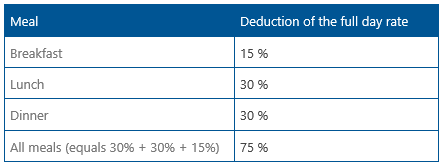

Meal deductions

If an employee is getting the Standard meal allowance and is treated for any of the meals, these meals must be deducted from the travel allowance. Some examples:

• You had breakfast on the hotel, and the entire invoice is refunded to you from your employer. You should then deduct the breakfast from all the days.

• You had a meeting with a client, and you paid the lunch. Then you would ask for a refund from your employer for the lunch you paid for yourself and the client, with receipt, and then deduct the lunch from the allowance that day.

• You had a meeting with a supplier, and they treated you for dinner. Then you should deduct Dinner from that day’s travel allowance.

Accommodation Allowance

The employee gets an allowance for each full day (24 hours).

This means that:

• If the trip lasted for 23 hours and 59 minutes, the employee is not entitled to accommodation allowance.

• If the trip lasted for 24 hours and 0 minutes, the employee gets: One full day.

• If the trip lasted for 47 hours and 59 minutes, the employee gets: One full day (gets for each completed 24 hour)

• If the trip lasted for 48 hours, the employee gets: Two full days

Documentation

For the allowance to be tax-free, the following must be documented, and hence specified on the settlement report.

• Business purpose and target (Formål og delmål) of the trip.

• Number of days on the trip.

• Start and end date and time.

• Calculation of the allowance.

• What rate has been used

References

• SKAT: Skattefri rejsegodtgørelse (diæter)

• TAX.DK skat & afgift: Skattefri rejsegodtgørelse

• SKAT: C.A.7.2.7 Dækningsprincip for rejseudgifter (udlæg efter regning eller godtgørelse)

Comments